In the realm of wealth management, particularly for the astute and financially accomplished, the conversation around estate planning often gravitates towards the federal estate tax, a topic rife with complexity and concern. Yet, it’s the state-level estate and inheritance taxes that frequently catch our clients off-guard, particularly those who, like many we have the privilege of advising, reside or hold assets in Illinois. This oversight is understandable but can have significant implications for estate planning strategies.

As fiduciaries dedicated to the sophisticated management of wealth, we navigate these waters with a keen eye on both the broader horizon and the minutiae that could impact our clients’ legacies. In Illinois, the estate tax landscape presents unique challenges and opportunities for those entrusted with substantial assets. Here, we delve into the Illinois estate tax, highlighting four crucial aspects that, in our experience, are pivotal for comprehensive estate planning.

Illinois Estate Tax: A Primer for the Informed Investor

1. $4 Million Exemption and the Absence of Portability

Illinois sets its estate tax exemption at $4 million, a threshold that, while generous, can be quickly surpassed by the assets accumulated by high-achievers. Unlike the federal exemption, Illinois does not offer portability between spouses—a “use-it-or-lose-it” scenario that demands strategic planning. For married couples with estates in the realm of $8 million, the distinction between utilizing individual exemptions through careful estate structuring versus the potential tax implications of a single, combined estate cannot be overstated. Incorporating credit shelter or “bypass” trusts can prove instrumental in maximizing each spouse’s exemption, a strategy that exemplifies the nuanced planning required to navigate Illinois’s unique tax landscape effectively.

2. Understanding Illinois’s Regressive Estate Tax Rates

At first glance, Illinois’s estate tax rates, ranging from 0.8% to 16%, suggest a progressive structure. However, the reality is more complex, with the actual rates applied in a regressive manner after a detailed computation. This nuance underscores the importance of advanced planning and the use of specialized tools, such as the Illinois Attorney General’s estate tax calculator, to accurately anticipate the tax implications for estates of varying sizes. Moreover, Illinois estate taxes can be deducted from the federal taxable estate, an aspect that should be integrated into broader tax mitigation strategies.

3. The Impact of Prior Taxable Gifts

Illinois’s approach to taxable gifts adds another layer of complexity to estate planning. While gifts made during one’s lifetime are not directly taxed by the state, they are considered when calculating the estate tax if they exceed the annual exclusion amount. This inclusion can significantly affect the estate’s tax liability, illustrating the strategic value of lifetime gifting as part of a holistic estate planning approach. Particularly, inter vivos gifts can mitigate the estate tax burden more effectively than testamentary gifts, provided they are structured to align with Illinois’s unique tax calculation methods.

4. Non-Residents and Illinois Property

For those residing outside Illinois but owning property within the state, the estate tax can present unexpected challenges. Illinois taxes the estates of non-residents based on the value of their Illinois property, requiring careful planning to minimize the tax impact. Conversely, Illinois residents with property in states without an estate tax must also navigate the complexities of Illinois’s tax calculations. Strategies involving LLCs or other mechanisms to classify tangible assets as intangible may offer pathways to tax mitigation, underscoring the importance of specialized legal advice in these scenarios.

Navigating the Non-Portability Challenge for Couples

A critical distinction that sophisticated investors must grasp is the contrast between federal and Illinois estate tax exemptions, especially regarding portability. Federal law allows for the portability of the estate tax exemption between spouses, enabling the surviving spouse to utilize any unused portion of their deceased spouse’s exemption, thereby minimizing their potential federal estate tax burden. However, Illinois does not afford this flexibility. The Illinois estate tax exemption lacks portability, creating a scenario where strategic use of each spouse’s exemption is not just advantageous but necessary. This ‘use-it-or-lose-it’ characteristic demands careful planning to ensure that none of the exemption goes to waste.

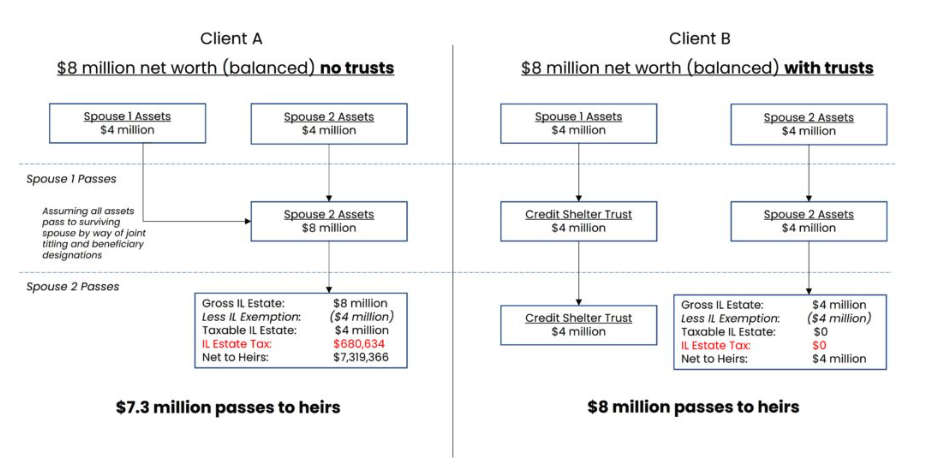

To elucidate the significance of this difference for couples with substantial assets—consider a couple with a net worth of $8 million. The absence of exemption portability in Illinois can profoundly influence their estate planning strategy, as illustrated by the forthcoming flow charts.

The critical insight derived from our analysis underscores the necessity for clients to strategically balance their assets between spouses and to thoughtfully integrate credit shelter or “bypass” trusts into their estate planning framework. Consider two hypothetical clients, each with an estate valued at $8 million. For Client B, a sophisticated estate plan has been meticulously crafted, incorporating trusts for both spouses. This strategy ensures that upon the passing of the first spouse, $4 million is allocated to a trust for the surviving spouse’s benefit, utilizing the Illinois estate tax exemption effectively.

Consequently, the surviving spouse retains $4 million in personal assets, complemented by an additional $4 million safeguarded within a credit shelter trust, thus completely mitigating any Illinois estate tax liability upon their demise. In stark contrast, Client A’s approach—directly assigning all assets to the surviving spouse—results in a significant Illinois estate tax of $680,634 on an identical $8 million estate. This comparison vividly illustrates the profound impact of strategic estate planning in navigating the complexities of Illinois’s estate tax landscape.

Navigating Illinois Estate Tax: A Path Forward

The intricacies of Illinois estate tax underscore the need for vigilant, informed estate planning. For our clients, this means not just understanding the landscape but actively engaging in strategies designed to preserve wealth and legacy. Our role, as stewards of your financial well-being, is to guide you through these complexities, ensuring that your estate plan not only meets legal requirements but also aligns with your vision for the future.

As always, we recommend consulting with your estate planning attorney to tailor these strategies to your specific situation. The landscape of estate tax, both federal and state, is ever-evolving, and staying abreast of these changes is paramount to effective wealth management. In our ongoing commitment to your financial success, we remain at the forefront of these discussions, ready to adapt and advise on the best paths forward for you and your heirs.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. The above is legal information is provided for educational purposes only, individuals should reach out to a qualified legal professional based on their own circumstances. Certain information is based upon third party data and may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy or confirmed the adequacy of this article. The opinions expressed by featured authors are their own and may not accurately reflect those of Cogent Strategic Wealth®

Recent Articles

Share:

Liz Winkle’s Five-Year Milestone: A Legacy of Dedication and Excellence

Share: